The Real Estate industry is valued at $280 trillion globally. In the modern world this industry continues to be influenced and shaped by growth in population, increase in migration rates, and lifestyle choices, apart from global macroeconomic factors. Property continues to be an important asset class in many countries, and irrespective of slowing economies or declining real estate markets, its status as a valued asset is among the top in such regions. As the economic uncertainty around the global real estate market rises, technology is seemingly the splint that can hold the industry together in the coming years. Although the industry has started to adopt technology in some form or shape in the various stages of the lifecycle, the sector is ripe for innovations to step in at an even higher scale.

Technology has helped real estate to grow beyond just offering traditional brick-and-mortar products and related services. The industry has traditionally been built on tangibility and steadiness and when coupled with technology, an ever-evolving and intangible force, beckons a synergy that not only has an economic impact but social ones as well. One of the best examples for this would be of the shared economy. Concepts like co-living, co-working, and co-owning have helped in offering more than just economical and convenient options. AI, automation, and robotics hold the potential to make construction less labor intensive. Drones and spatial intelligence are helping in surveying and inspection in all phases of development. Real estate marketplaces have become household terms and managing a property is taking a mobile-first approach. Technology has invariably created new opportunities in the real estate lifecycle – to enhance the processes, reduce the risks involved, increase the quality of the final product and enhance the quality of customer service.

The use of technology in every phase in the development and maintenance of properties, from surveying to facility management, is evident. Surveying, Architecture & Design, Construction, Sales & Marketing, and Property Management are key functionalities where technology is leaving a mark. Homes are getting smarter, work spaces are being shared, and monitoring of construction sites in real time is not an uncommon practice. But has the use of technology reached its saturation point in any of the phases involved in the development of a real estate product?

The use of technology in every phase in the development and maintenance of properties, from surveying to facility management, is evident. Surveying, Architecture & Design, Construction, Sales & Marketing, and Property Management are key functionalities where technology is leaving a mark. Homes are getting smarter, work spaces are being shared, and monitoring of construction sites in real time is not an uncommon practice. But has the use of technology reached its saturation point in any of the phases involved in the development of a real estate product?

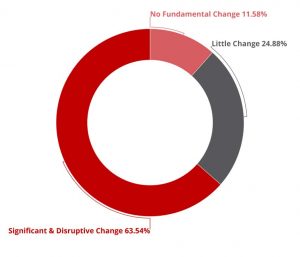

More than 60% of the respondents of the global PropTech Time survey 2019 conducted by HexGn believe that technology still has scope to create significant and disruptive changes in the coming years, clearly indicating that those in the field still feel that the pinnacle of technology is yet to come.

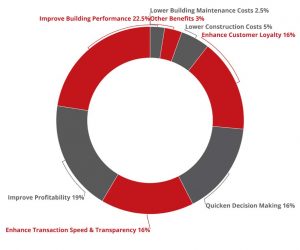

With investment trends seeming favorable towards the technology industry, there is also the question of whether technology is helping achieve higher revenues or is it just making the industry smarter and more advanced without the much-needed economic benefits. The use of technology to make different realms in the real estate product lifecycle easier and more efficient comes at the cost of acquiring the means to use these technologies. It therefore becomes imperative to look at how these technologies is helping its users. Traditionally the Real Estate industry focused more on reducing the cost of creating the tangible product, and most efforts were spent in looking for technically advanced construction methods that would reduce cost and save time. However, today the real estate professionals are looking at technology to address other business aspects such as improving building performance, quicken transaction process, increase transparency, quicken decision making using data, and enhancing customer loyalty. Technologies has changed the way each phase is completed by arming professionals with a number of data- driven tools. Data is proving to be the king. But, the lack of resources to understand the ways to harness the data has caught the attention and has been the fueling factor driving the jobs market as startups and real estate companies look for the talent they need to address this need.

While investments crossing $24 billion in 2018 globally and a market of more than $500 billion are fantastic indicators when it comes to the growth of technology, they are not necessarily an indicator of how well the revenues in the real estate industry has surged owing to the real estate technologies. The investments are growing and aptly so, as many of the technology services require a sound digital infrastructure and tools – all of which require a sound capital backing. The expense of getting the basic infrastructure for real estate technologies to grow is also a prominent challenge as startups and technology companies find it a challenge to convince their potential audience that the investment is worth it, and that the services provided are cost-effective. Those failing to spot opportunities to become tech-driven stand as a testament to the increasing rate of stagnation or failure resulting from not keeping up with fast-evolving industry. Those that are making efforts, are doing it through increased spending in the form of acquiring or investing in startups. Being associated with such startups has been a good way of ensuring a head start in the niche by discovering new technologies and becoming pioneers in it in the mainstream industry.

The larger picture of technology and real estate industries converging cannot be understood without understanding the role of profitability and risk assessment. Adopting technology offers higher quality of risk assessment results but there is also the need to assess the risk surrounding the adoption of any technology. Factors such as its effect on the business and the people involved in it becomes crucial. Leaders, in real estate segment wanting to introduce new tech applications to bring changes in the way the business is run, also deal with the issue of resistance from team members. This may again be due to the changes in team functionalities that accompany the new technologies and the fear of losing jobs. Some of these pose the risk of turning an employee’s contribution redundant too, at times. As per the global PropTech Time survey 2019, conducted by HexGn, more than 50% of the respondents across the lifecycle and at different hierarchies feel that robots will perform their job in the next ten years. Some of the most resisted technology is that of AI, machine learning and robotics – all three infamous for threatening manual labor jobs in all industries. However, these technologies can be grown to become an important pillar in the industry and can create newer jobs. Today, accessibility factors and sustainability needs hold the key to organize and drive technology’s role in real estate.

The larger picture of technology and real estate industries converging cannot be understood without understanding the role of profitability and risk assessment. Adopting technology offers higher quality of risk assessment results but there is also the need to assess the risk surrounding the adoption of any technology. Factors such as its effect on the business and the people involved in it becomes crucial. Leaders, in real estate segment wanting to introduce new tech applications to bring changes in the way the business is run, also deal with the issue of resistance from team members. This may again be due to the changes in team functionalities that accompany the new technologies and the fear of losing jobs. Some of these pose the risk of turning an employee’s contribution redundant too, at times. As per the global PropTech Time survey 2019, conducted by HexGn, more than 50% of the respondents across the lifecycle and at different hierarchies feel that robots will perform their job in the next ten years. Some of the most resisted technology is that of AI, machine learning and robotics – all three infamous for threatening manual labor jobs in all industries. However, these technologies can be grown to become an important pillar in the industry and can create newer jobs. Today, accessibility factors and sustainability needs hold the key to organize and drive technology’s role in real estate.

These technologies and those that help in offering better access to various aspects of real estate products are already multiplying in applications. The new waves of technology are about creating unmatched access and using it to improve the various functions and can be accredited to technologies like AI, machine learning, and IoT among the others. From construction to energy consumption, the deep tech applications have piqued the interests of real estate and technology stakeholders across the globe. An important aspect that those adopting technology must focus on is to find the best applications amid the sea of options and get only those technologies on board that are needed to ensure cost effectiveness. This becomes crucial as real estate technologies develop and emerge actively, creating a wide pool of options for the users. Filtering out of the ‘noise’ and choosing only what is required increases the effectiveness and contribution of technology in fueling sales and not just in enhancing the processes.